Executive summary – what changed and why it matters

BloombergNEF now projects planned U.S. data-center capacity will raise electricity demand from about 40 GW today to 106 GW by 2035 – roughly 2.7x the sector’s current draw. The shift is driven by much larger facilities (average new sites >100 MW; ~25% >500 MW; a few >1 GW) and rising utilization as AI workloads approach ~40% of total compute.

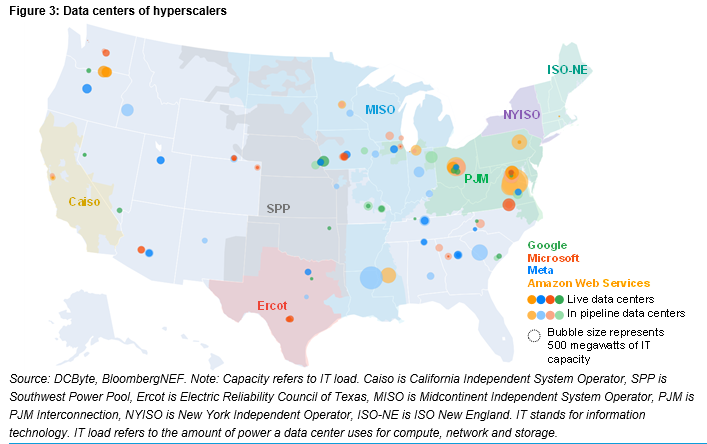

- Impact is concentrated: most new builds are in PJM and ERCOT footprints (Virginia, Pennsylvania, Ohio, Illinois, New Jersey, Texas).

- Grid and regulatory stress is already appearing: PJM’s independent monitor has asked FERC to enforce interconnection constraints and create a load queue.

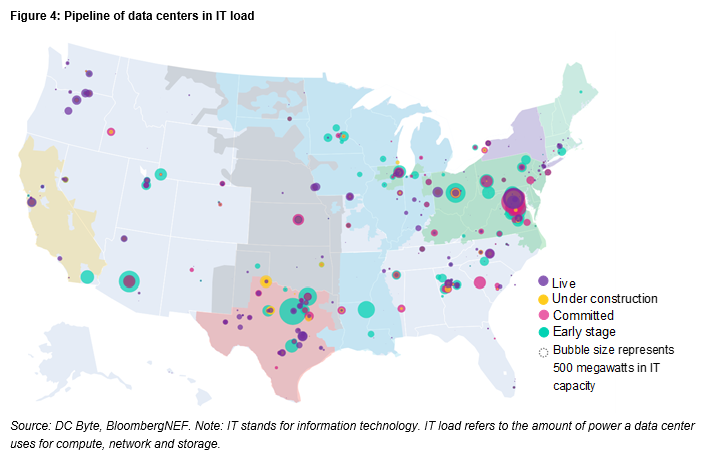

- Timing matters: early-stage project announcements doubled between early‑2024 and early‑2025, and with ~7 years to build, later-stage pipeline revisions materially change the 2030s tail.

Key takeaways for executives and product leaders

- Scale and density: The average new facility will exceed 100 MW, skewing investment toward fewer, much larger campuses. That changes procurement, interconnection, and siting strategy.

- AI is a utilization multiplier: Forecasted utilization rises from 59% to 69% as AI training/inference climbs to ~40% of compute, increasing peak and sustained loads.

- Regional risk: Concentration in PJM and ERCOT creates local transmission, capacity, and price risks – not just national-level capacity concerns.

- Policy and interconnection: Monitoring Analytics has petitioned FERC arguing PJM must limit new connections until capacity is proven; interconnection could become a gating factor.

Breaking down the announcement — numbers and immediate consequences

BloombergNEF’s headline numbers: 40 GW today → 106 GW by 2035; planned facility sizes shifting from a market where only ~10% draw >50 MW today to an environment where the average new site is well over 100 MW, nearly 25% exceed 500 MW, and a handful top 1 GW. Utilization grows from 59% to 69% as AI consumes ~40% of compute. The group also points to global facilities investment hitting ~$580 billion this year, underscoring capital intensity.

Two important dynamics amplify risk: project concentration (geographic clustering) and project timing. Early-stage projects more than doubled year-over-year, and with a typical seven-year build-to-service timeline, the pipeline’s shape today has outsized influence on 2035 outcomes.

Grid and regulatory implications

Concentrated demand in PJM and ERCOT will stress transmission corridors, local capacity markets, and interconnection queues. Monitoring Analytics (PJM’s independent market monitor) has filed with FERC urging PJM to require large data-center loads to wait until reliable service can be guaranteed and to create a formal load queue — essentially asking for stricter gating of new connections. The monitor also tied rising prices in the region partially to data-center demand.

Practically, that can mean longer lead times, requirement for network upgrades paid by developers, and potential curtailment/limiting of new load until transmission is expanded. For utilities and grid planners, this shifts the budgetary focus toward large transmission upgrades and fast-track capacity planning.

Business implications — who wins, who should pause

Data-center operators with deep utility relationships and flexibility tools (on-site generation, storage, long-term PPAs, demand-shift capability) gain advantage. Colocation providers who can secure transmission rights and staged build plans will outcompete speculative greenfield entrants. Utilities and transmission developers could capture substantial build revenue but face political and permitting risk.

Conversely, projects dependent on fast, low-cost interconnection may be delayed or become more expensive. Local communities and regulators will demand clearer commitments on grid impacts, taxes, and workforce benefits.

Recommendations — immediate actions (practical)

- Model worst-case load scenarios: Update capacity planning to reflect 2.7x demand growth and higher utilization; stress-test for concentrated regional growth.

- Prioritize interconnection certainty: Secure early-stage transmission agreements, accept staged build commitments, and budget for network upgrade cost-share.

- Invest in flexibility: For operators, pair projects with on-site storage, gas peakers or firmed renewables and contracts that allow for demand response and load shaping.

- Engage regulators proactively: Utilities, developers, and local governments should jointly map cumulative impacts and publish mitigation plans before projects reach FERC or RTO hearings.

Bottom line

BloombergNEF’s revision is a directional alarm: planned data-center electricity demand could nearly triple by 2035, concentrated in a handful of grid regions. That creates tangible commercial opportunities for transmission developers and utilities — and material risks for operators who underprice interconnection, overlook utilization increases from AI, or assume unobstructed permitting. Executives should treat interconnection and grid services as core project risks, not afterthoughts.

Leave a Reply