What Changed-and Why It Matters

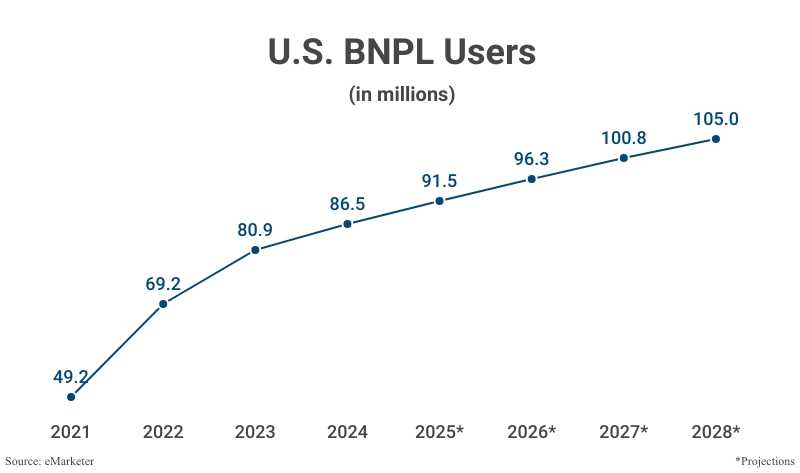

BNPL moved from discretionary buys to essentials: 91.5 million U.S. users and roughly 25% now using it for groceries. Late payments are rising-42% of BNPL users made at least one late payment in 2025 (up from 39% in 2024 and 34% in 2023, per survey data). The structural problem: most BNPL loans aren’t reported to credit bureaus, creating “phantom debt” that other lenders can’t see. That invisibility elevates spillover risk into credit cards, auto, and student loans.

This matters now because BNPL is embedded into mainstream rails (Apple Pay, Google Pay, major processors), while federal oversight has softened and states are filling the void inconsistently. The result is a fast-growing, lightly visible credit channel used by financially strained borrowers. It’s not 2008-scale, but the concentration and opacity are red flags for lenders, retailers, and fintech operators.

Key Takeaways

- BNPL usage for essentials is up; late payments hit 42% in 2025-stress is mounting.

- “Phantom debt” blinds underwriting: many loans aren’t reported, and concurrent borrowing is common.

- Federal enforcement has been rolled back; state-by-state rules create regulatory arbitrage.

- Spillover risk: borrowers often keep BNPL current while larger debts go delinquent.

- BNPL is expanding into B2B; trade credit is a $4.9T market—amplifying potential knock-on effects.

Breaking Down the Risk

Public data paints an uncomfortable picture. A federal analysis of major BNPL providers showed 63% of borrowers had multiple simultaneous loans in a year and 33% borrowed across multiple lenders. Roughly one-fifth were “heavy users,” averaging more than one BNPL loan each month. Approval rates remain high even among subprime and deep subprime applicants (reported around 78%).

BNPL loans are small and often repaid first because they are short-term and visible at checkout; that can make portfolios look fine while masking broader distress. Credit cards, auto, and student loans may deteriorate first, giving banks and issuers a distorted signal until losses arrive. A regional Federal Reserve bank has flagged this “spillover” channel as the real systemic concern—not BNPL balances themselves.

Why Now: Macro and Market Timing

Consumer stress indicators are mixed but deteriorating at the margin: unemployment ticked up toward 4.3%, auto delinquencies have worsened for subprime cohorts, and student loan payments restarted with millions already delinquent or in default. Meanwhile, BNPL has gone mainstream: Affirm reports nearly 2 million debit cardholders financing in stores, and PayPal processed about $33 billion in BNPL spending in 2024, growing ~20% year over year. Integration via Apple Pay, Google Pay, and large processors pushes invisible installment credit into everyday transactions—even at the grocery checkout.

Next, expect acceleration in B2B BNPL. Trade credit among U.S. firms is roughly $4.9 trillion in payables; some B2B BNPL providers report small-business spend rising ~40% upon access. That’s commercial growth—and risk—flowing into a channel with even less standardized reporting.

Governance and Data Gaps

Regulatory whiplash widened the visibility gap. An effort to apply credit card-like protections to BNPL under the Truth in Lending Act stalled; the agency later highlighted high repayment rates among first-time BNPL users and no causal link to debt stress. That narrower lens misses cohort risk: what happens as borrowers stack loans across apps over time. New York’s licensing regime is a start, but patchwork rules enable arbitrage. Bottom line: underwriting models—especially AI-driven ones—are operating with blind spots because material BNPL exposure never hits traditional bureaus.

Competitive Angle: BNPL vs Card Installments vs Personal Loans

BNPL wins on checkout friction and perceived 0% pricing, often subsidized by higher merchant fees in exchange for conversion and basket lift. Card “installments” and personal loans offer clearer bureau reporting and established dispute rights, but add friction and interest costs. For merchants, BNPL lifts conversion but may cannibalize higher-margin card volume and introduce operational risk if customers rely on BNPL for staples. For banks, expect rising card charge-offs even if BNPL performance looks superficially stable.

What Operators Should Do Now

- Retailers and marketplaces: segment essentials (e.g., groceries) and consider throttling or limiting BNPL on staple SKUs; monitor AOV and repeat purchase lift versus late-payment rates and support costs.

- BNPL providers and processors: implement hard caps on concurrent loans, require real-time income and affordability checks on essentials, and commit to bureau or registry reporting (even if voluntary) to reduce “phantom debt.”

- Banks and card issuers: incorporate BNPL signals via alternative data partners; adjust line management and early-warning triggers to reflect that BNPL is likely prioritized over card payments.

- Fintech risk leaders: stress test heavy-user cohorts with stacked loans; build cohort-level PD/LGD views rather than first-loan metrics; document model limitations for governance.

- CFOs of SMBs exploring B2B BNPL: set policy limits by vendor and term; reconcile BNPL payables weekly; simulate cash‑flow shocks if terms compress or fees rise.

- Policy teams: plan for a national registry or standardized reporting framework; in the interim, maintain multi-state compliance inventories to avoid gaps.

Bottom Line

BNPL’s shift into essentials, rising late payments, and the persistence of “phantom debt” create a visibility problem at exactly the moment adoption is peaking. This isn’t a 2008-scale threat, but the spillover into traditional credit could arrive quickly and unevenly. Enterprises should tighten affordability checks, seek cross-lender visibility, and prepare for higher card and auto delinquencies even if BNPL books appear orderly. Treat BNPL as credit infrastructure—not a marketing feature—and manage it with the same rigor.

Leave a Reply