Traton’s megawatt-charging push turns the EU’s 2040 diesel phase-out into a fleet cost advantage

Why it matters: As the EU forces a 90% CO2 cut for heavy-duty trucks by 2040 and interim targets start hitting, Traton (Scania, MAN, International) is moving from pilot to scale. It’s ramping electric truck production, standing up battery plants, and building a Europe-wide public charging network with megawatt-class chargers via Milence-compressing timelines and costs for freight operators and reshaping the competitive map.

Executive Summary

- Speed to scale: MAN’s new flexible line builds diesel and electric on the same line, lowering unit costs as volumes rise; Scania’s long-haul EVs near 350 miles per charge.

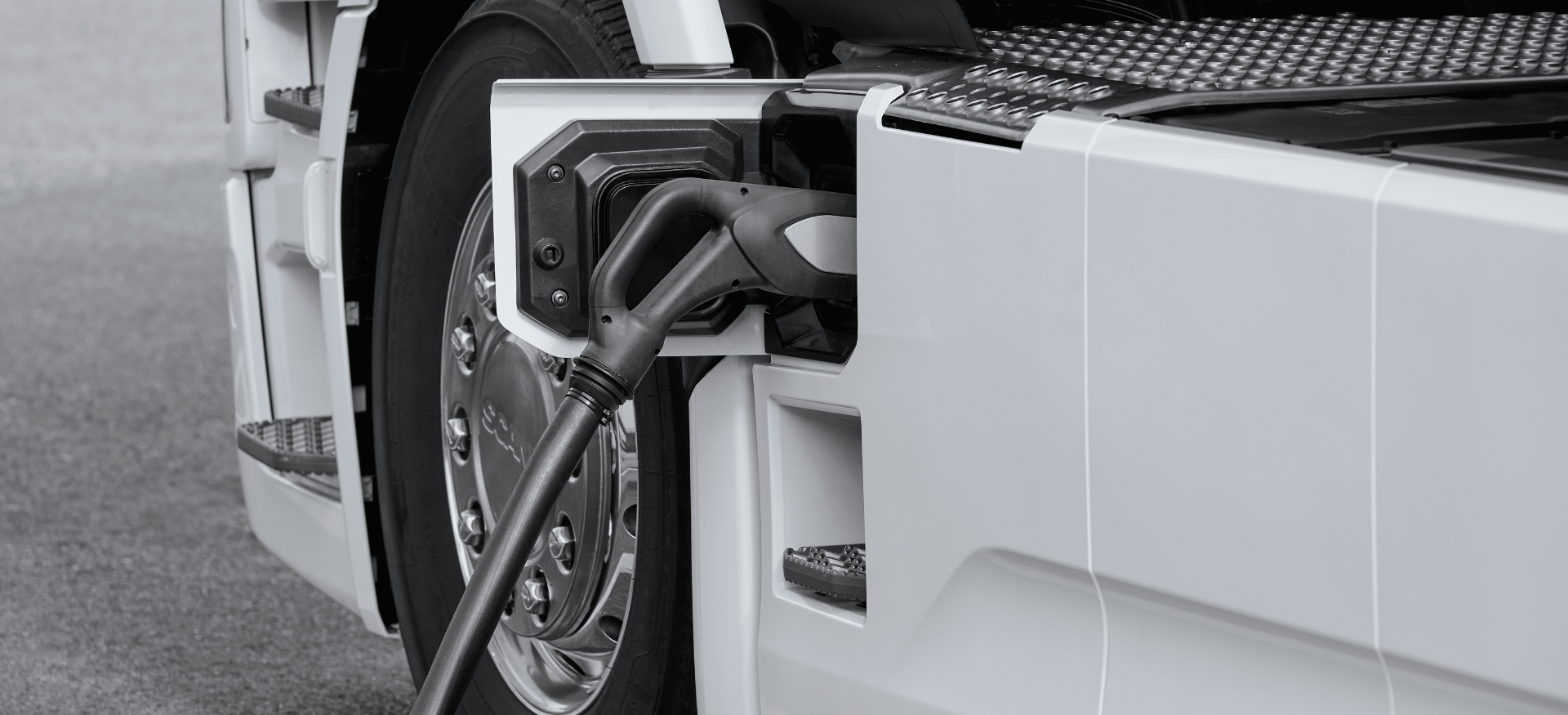

- Infrastructure unlock: Milence is deploying public megawatt chargers (1+ MW) enabling ~45-minute turnarounds, essential for long-haul duty cycles.

- Regulatory tailwinds: EU heavy-duty CO2 rules phase out new diesel by 2040; H1 2025 EV sales at Traton doubled to 1,250, signaling acceleration.

Market Context

Freight is roughly 8% of global greenhouse emissions, with trucks and vans responsible for about 65% of that. The International Council on Clean Transportation estimates battery-electric trucks in Europe already cut emissions by ~63% versus diesel on average, factoring today’s grid mix. Last year saw ~90,000 electric truck sales globally, still <2.5% penetration, but growth is inflecting as policy, tech, and infrastructure align.

Traton’s trajectory puts it in the first rank with Volvo and other European incumbents, while Chinese OEMs expand internationally with cost-competitive offerings. The risk side: battery constraints (a heavy truck needs 4-6 car-equivalent packs), fierce price competition, and policy uncertainty in the U.S. for Traton’s International brand. To mitigate supply risk, Traton is building battery capacity in Sweden and Germany targeting 50,000 packs/year (enough for ~10,000 trucks).

Opportunity Analysis

- Total cost of ownership (TCO): Flexible factories and rising volumes should narrow upfront price gaps; lower energy and maintenance can swing lifecycle costs in favor of EVs on high-utilization routes.

- Operational resilience: Public megawatt charging reduces reliance on depot-only infrastructure, enabling mixed-route and back-to-back operations.

- Revenue upside: Shippers are prioritizing low-carbon lanes; EV capacity can command premiums in RFPs and secure longer-term contracts.

- Capital leverage: EU funding and national incentives can offset grid upgrades and chargers, improving payback on early deployments.

- Data advantage: Electrified fleets generate richer telematics for energy management, battery health, and carbon reporting-valuable for ESG and customer audits.

Action Items

- Run a 12-18 month pilot on 2-3 lanes aligned to Milence sites; validate dwell, charging windows, and driver scheduling with megawatt-capable vehicles.

- Lock supply: Secure multi-year allocations for trucks and battery packs; include performance guarantees and residual value protections.

- Energy strategy: Negotiate renewable PPAs or hedges for depot charging; integrate smart charging and demand-response to cut peak costs.

- Infrastructure co-invest: Apply for EU/Member State funds; co-locate public megawatt chargers at logistics hubs to monetize downtime and support partners.

- Operations upskilling: Train drivers and technicians on high-voltage safety and EV driving efficiency; update maintenance and parts inventory.

- Sales and procurement: Embed low-carbon capacity in bids; quantify CO2 reductions per shipment to win sustainability-driven contracts.

- Scenario planning (U.S.): For International-branded operations, model tariff and policy swings; diversify routes and financing to cushion demand shocks.

- KPIs and governance: Track TCO per lane, charger utilization, battery degradation, and Scope 3 reductions; tie executive incentives to electrification milestones.

Near-term milestones: MAN targets 1,000 e-truck deliveries from its new line by year-end; Scania plans megawatt-charger-compatible heavy-duty sales from February, with deliveries later in the year; Milence has megawatt chargers live in Sweden, Belgium, and the Netherlands, with five more sites imminent. First movers will set lane standards-and pricing power—for low-carbon freight.

Leave a Reply