US EV Tax Credits Are Gone: Prepare for a Demand Cliff and Costlier Electrification

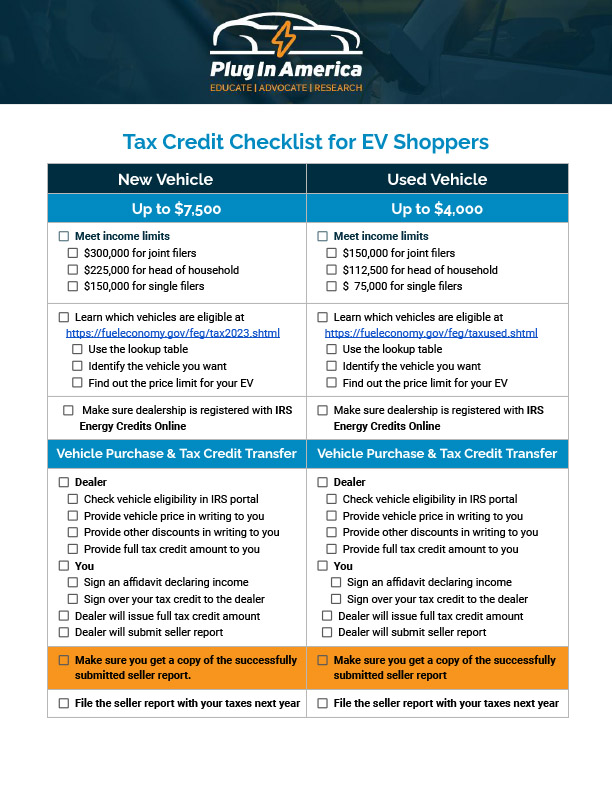

US federal EV tax credits from the Inflation Reduction Act officially ended Wednesday, removing up to $7,500 in purchase offsets that reduced upfront EV costs and boosted demand. Expect a near-term sales surge followed by a sharp decline, complicating automakers’ production planning, state incentive strategies, fleet electrification timelines, and progress toward national emissions-reduction targets.

Executive Summary

- Immediate demand whiplash: a short-term sales spike gives way to a slump that could cut EV share to low single digits before stabilizing.

- Pricing and margin pressure: effective prices rise up to $7,500, forcing OEMs and dealers into incentives, financing offers, and model mix shifts.

- Policy and planning risk: slower adoption threatens fleet targets and emissions goals; capital plans, supplier volumes, and charging ROI need re-baselining.

Market Context: A Playbook Written in Germany

Germany’s 2016-2023 EV subsidy cycle is the closest analog. Each pullback produced a predictable pattern: sales peak right before a cutoff, then crater after. When Germany ended incentives abruptly in December 2023, January 2024 BEV sales fell by roughly half. The US already saw the first act-EVs hit ~10% of new sales in August with analysts calling September a record-followed by an expected slump. One forecast cited in the Washington Post puts near-term US EV share at 1-2%.

Longer term, Germany’s BEV share slipped from 18.5% to 13.5% in 2024 before recovering somewhat in 2025. In the US, Princeton University’s Zero Lab estimates BEV sales could be about 40% lower in 2030 without federal credits. With road transport nearly a quarter of US emissions, slower EV uptake sets back climate progress and cedes ground to global leaders like China.

Opportunity Analysis: Who Gains, Who Hurts

Winners: cost leaders with flexible pricing, brands with strong hybrid lineups to bridge demand, and state-incentive-savvy players prioritizing ZEV markets (e.g., CA, CO, NJ, NY). Captive finance units able to subsidize monthly payments and used EV marketplaces stand to benefit, as buyers pivot to affordability and total cost of ownership.

At risk: premium EV-first brands with higher ASPs, suppliers tied to aggressive battery ramp curves, and charging operators whose utilization and payback assume faster EV penetration. Fleets facing budget cycles may defer electrification absent federal support, dragging on volume commitments and depot-charging projects.

Action Items: Defend Share and Margins Now

- Reprice and repackage: deploy targeted incentives, low-APR financing, and subscription bundles to offset the lost $7,500 at the monthly-payment level.

- Prioritize high-yield geographies: shift inventory and marketing to states with strong rebates and HOV/utility perks; align dealer spiffs accordingly.

- Optimize model mix: emphasize hybrids and lower-trim EVs; defer or stagger high-ASP EV launches until demand normalizes.

- Renegotiate supply: recalibrate 2025-2027 battery and component volumes; add price-adjustment clauses tied to demand milestones.

- Fortify fleet value props: refresh TCO models with real-world fuel and maintenance savings; offer guaranteed residuals and uptime SLAs.

- Re-baseline infrastructure ROI: revise charging buildout and utilization assumptions; phase capex with confirmed volume.

- Scenario-plan policy risk: model sales, emissions, and compliance under prolonged credit absence; prepare advocacy positions for federal or state policy tweaks.

- Instrument the funnel: track EV consideration, days-on-lot, and cross-shopping with hybrids weekly; set auto-triggered incentives when inventory exceeds thresholds.

Sources: MIT Technology Review (The Spark), Washington Post, Princeton University Zero Lab. Business takeaway: treat the credit sunset as a shock test for your EV P&L and supply chain-move fast on pricing, mix, and state-led demand capture while re-sequencing long-horizon investments.

Leave a Reply